What better way to understand concepts big and small than through data visualizations? In this blog series, we produce insightful visuals using data from the SLGL dataHub to provide commentary on themes related to economics and transportation. Follow us as we explore and engage with interesting ideas.

The U.S. administration has announced a 25% global tariff on automobiles (cars and light trucks) and certain auto parts (engines, transmissions, and electrical components), effective April 3 and May 3, 2025, respectively. The administration contends that the tariffs address concerns that imports from the EU and Japan, along with North American supply chain integration, have weakened the U.S. industrial base and exposed manufacturers to key component shortages. Notably, as components often cross borders between Canada, the U.S., and Mexico before final assembly, U.S.-made content of cars will be exempt from the tariffs.

The automobile industry is a key part of the Canadian economy, with specialized expertise developed through years of free trade and integrated cross-border supply chains. Interestingly, it was the tariffs on American-made cars that initially led to car assembly in Canada using U.S.-made parts until the 1960s. Subsequent trade agreements reducing tariffs, in exchange for domestic production of Canada-sold cars, led manufacturers to build single models for all of North America in specific plants with inputs sourced from multiple countries. Over the years, Canada’s car production has declined from more than 3 million units in 1999 to just over 1.3 million units in 2024.

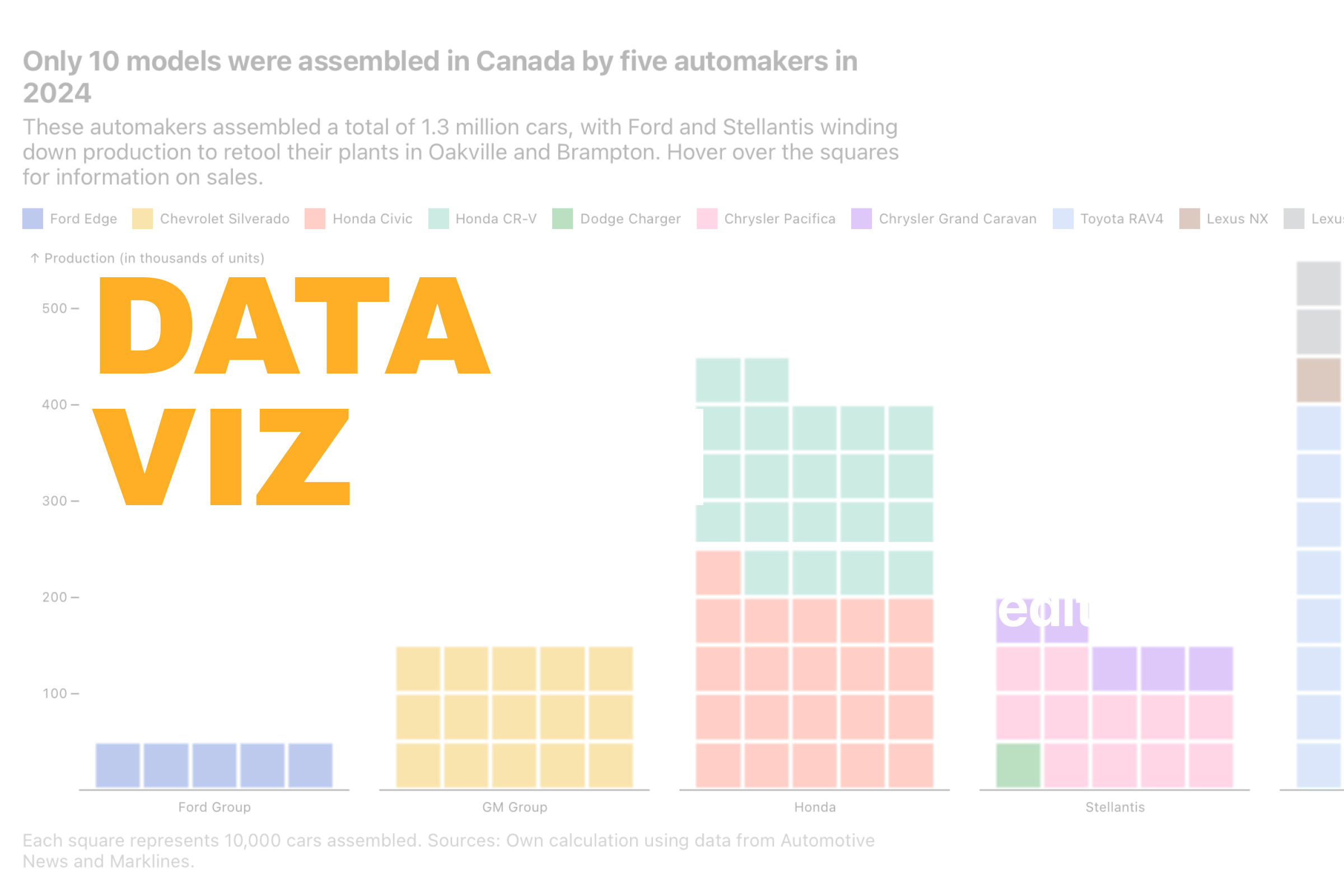

Consumer demand for car models fluctuates, as new iterations can be hit-or-miss, and retooling plants for different models is both costly and time-consuming. With the shift from internal combustion engines to EVs, some manufacturers have struggled to keep up, exposing them to market risks. Competing with mature EV technology from China, which are often aggressively priced, adds further pressure. In 2024, five carmakers had active assembly operations in Canada, producing 10 models. The model-plant strategy followed by manufacturers means most car models sold in Canada are imported, primarily from the U.S.

The charts show that of the 1.3 million cars assembled in Canada, the Toyota Group produced about 40% across three models manufactured in plants in Woodstock and Cambridge. Honda is the second-largest manufacturer, producing 31% with two models in Alliston. The remaining 29% is shared by the Ford Group, GM Group, and Stellantis, across five models. In terms of sales, only a quarter of the models produced in Canada were sold domestically in 2024, meaning these automakers are largely dependent on the U.S. market for sales of these models.

In conclusion, North America’s automotive industry depends on cross-border supply chains spanning Canada, the U.S., and Mexico, where inputs move seamlessly before final assembly under a model-plant strategy. The U.S. administration’s tariffs aim to address perceived vulnerabilities in the domestic industrial base, but in practice, they threaten to disrupt this intricate network. As components cross borders multiple times before final assembly, the tariffs would increase production costs, raising prices for consumers across North America, without solving the underlying issues within the supply chain.

Help us make this series even better! We would love to hear your thoughts and suggestions on content ideas and other noteworthy visualizations. Write to Bilal Siddika on LinkedIn or via email.